Kioxia Investor Day - Flash Memory Scales AI Inference

Investor Day 2026, June 2, 2026

Flash Memory Scales AI Inference

Kioxia’s Investor Day was a clear positive: the company raised its flash memory CAGR outlook to 22% (from 20%), demonstrated a laser-focused product strategy for AI inference workloads (CMX, Storage-Next, RAG), and gave investors a path to significant shareholder returns as it reaches net cash position in June.

5 KEY MESSAGES FROM INVESTOR DAY

1. NAND EB Demand CAGR Raised to 22% (vs. 20% Prior) — Modest but Credible Upgrade

Kioxia raised its CY25–28 flash memory EB (exabytes - 1000 GB) demand CAGR forecast from 20% to 22%, driven by stronger AI inference demand. Within DC (Data Center), inference-related demand grows at 86% CAGR (CY25–28E), with DC applications accounting for ~50% of total demand by CY28. Supply/demand remains tight through CY27.

2. Capital Investment Discipline: ¥470B/Yr FY27–29E — Only Modestly Above Plan

Planned capex for FY3/27–3/29 averages ¥470B/year, only modestly above the ¥450B FY3/27 plan. Annual front-end GB cost reductions targeted in the low-teens% range. Bit density targeted at +50%+ with each generation transition.

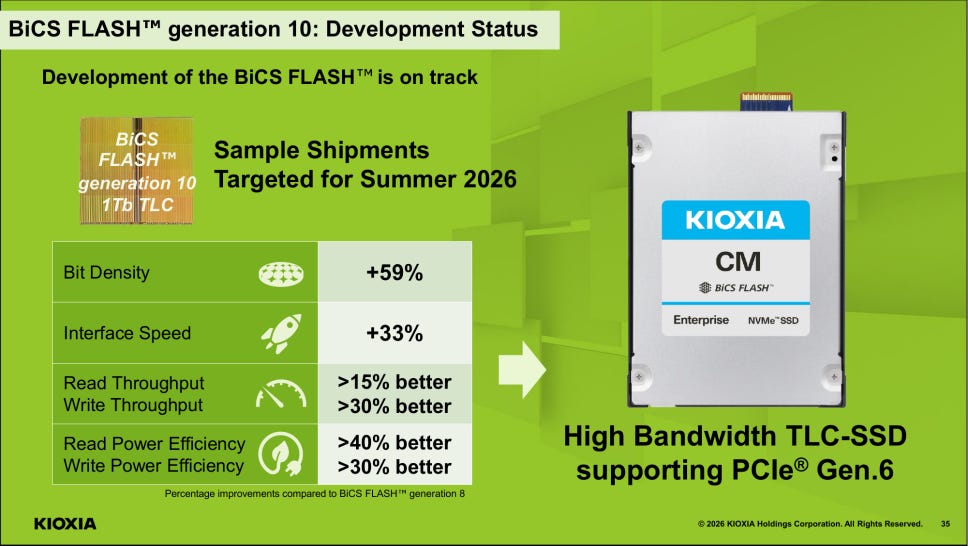

3. BiCS10: Samples Summer 2026, Mass Production ~Summer 2027; ~80% BiCS8 by FY3/27-end

BiCS10 targets samples in summer 2026 and mass production approximately one year later. BiCS8 is ramping now; ~80% of annual GB shipments expected to transition to BiCS8 by end of FY3/27. BiCS9 targets AI PCs/mobile; BiCS10 targets enterprise/data center with focus on higher capacity.

4. Progressive Dividend from FY3/28; Could Start in 2H FY3/27 if Cash Exceeds Expectations

Management is considering a progressive dividend from FY3/28 based on accumulated excess FCF generated through FY3/27. If cash generation exceeds expectations, dividends could begin in 2H FY3/27. CFO Kawamura added that if M&A is delayed, it would theoretically be possible to return all excess FCF to shareholders.

SECTION 1 — FLASH MEMORY MARKET OUTLOOK, SUPPLY-DEMAND and SSD FAMILIES

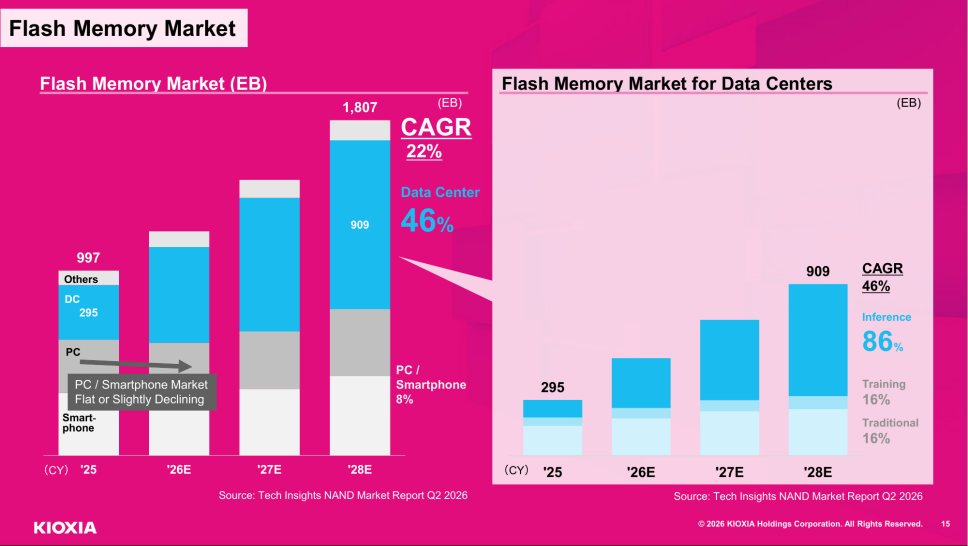

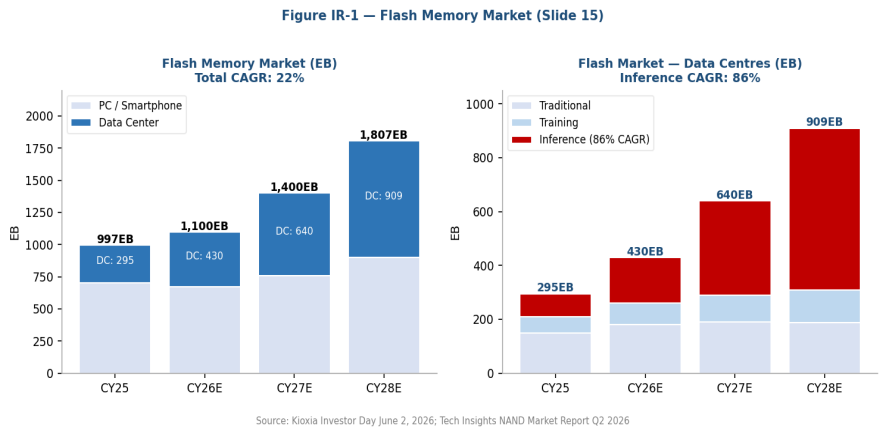

Investor Day Slide 15 — Flash Memory EB Market: Total CAGR 22% (↑ from 20% prior) | DC CAGR 46% | AI Inference CAGR 86% | PC/Smartphone flat-to-declining (Source: Tech Insights NAND Market Report Q2 2026)

The flagship market slide shows the structural demand shift underpinning the repricing cycle. Total flash demand grows from ~997 EB (CY25) to 1,807 EB (CY28), CAGR 22% (raised from 20%). Data centre is the growth engine: 295 EB in CY25 to 909 EB in CY28 (CAGR 46%). Within DC, inference (Agentic AI, Physical AI, RAG, KV-cache) grows at 86% CAGR vs. training at 16% CAGR. PC and smartphone NAND are flat to declining. PC/Smartphone — the driver of all prior NAND cycles — is flat or declining.

Figure IR-1 | Source: Kioxia Investor Day June 2, 2026; Tech Insights NAND Market Report Q2 2026

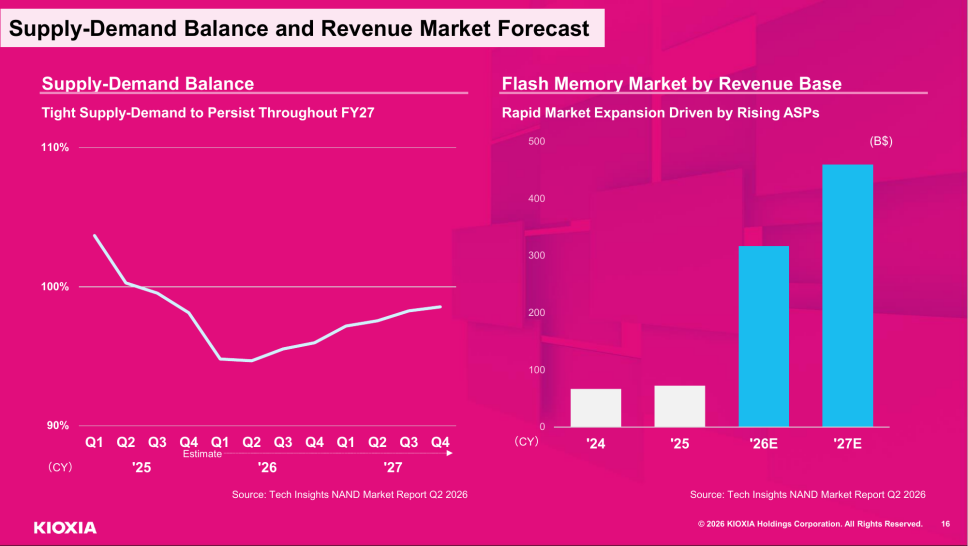

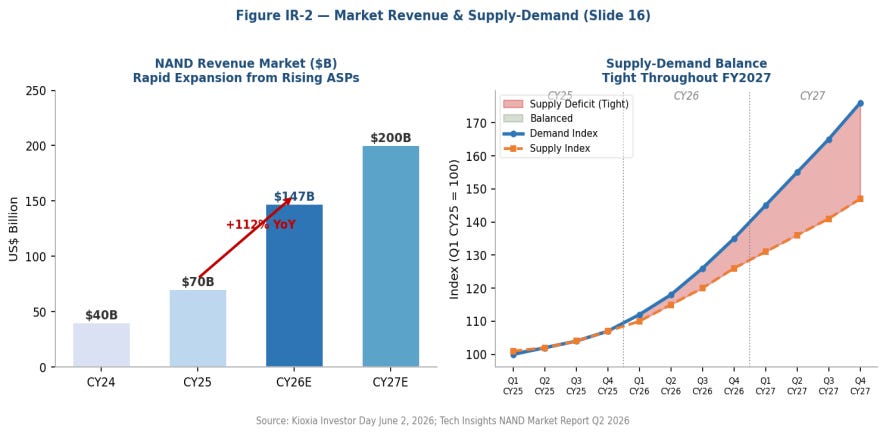

Investor Day Slide 16 — Supply-Demand Balance (L): Persistent deficit through Q4 CY27 | Revenue Market Forecast (R): US$147B CY26E (+112% YoY) → ~US$200B+ CY27E (Source: Tech Insights Q2 2026)

The supply-demand chart is the most important IR Day disclosure. The industry is in deficit from Q3 CY25 through Q4 CY27 — Kioxia’s entire CY26 capacity has been booked under LTAs. The revenue market bar chart shows a non-linear step: ~US$40B (CY24) → US$70B (CY25) → US$147B (CY26E, +112%) → US$200B+ (CY27E). Average NAND price per GB roughly doubles in CY26 alone, with further appreciation in CY27. US$-based GB ASP forecast to +215% YoY for FY3/27 (from +187% prior), with FY3/28 cut to -10% (from -16% prior) — reflecting management’s comments on LTA discussions extending into CY29 and beyond.

Figure IR-2 | Source: Kioxia Investor Day June 2, 2026; Tech Insights NAND Market Report Q2 2026

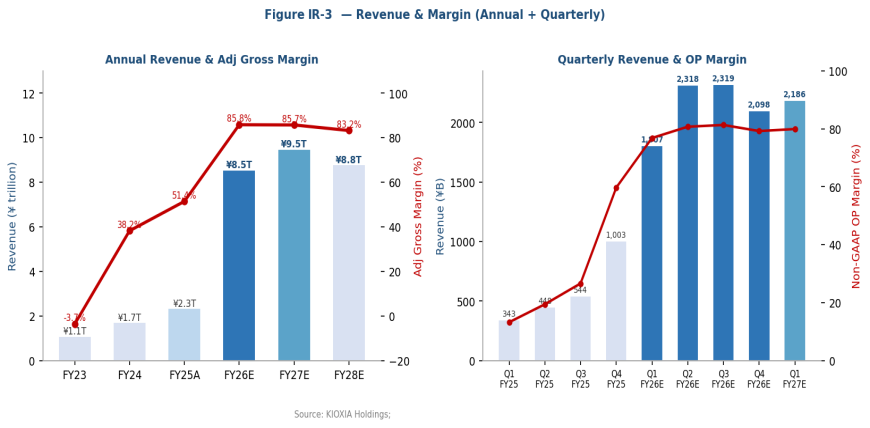

Figure IR-3 — Annual Revenue/GM and Quarterly Revenue/OPM trends | Source: KIOXIA Holdings

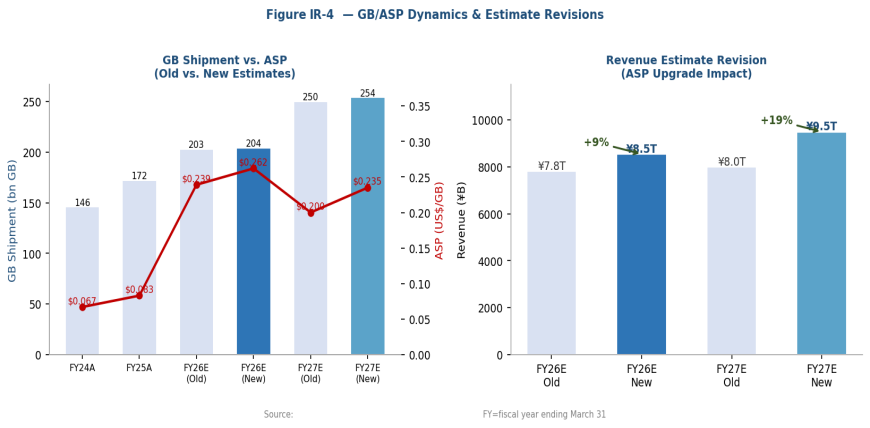

Figure IR-4 — GB Shipment/ASP old vs. new estimates & revenue revision impact

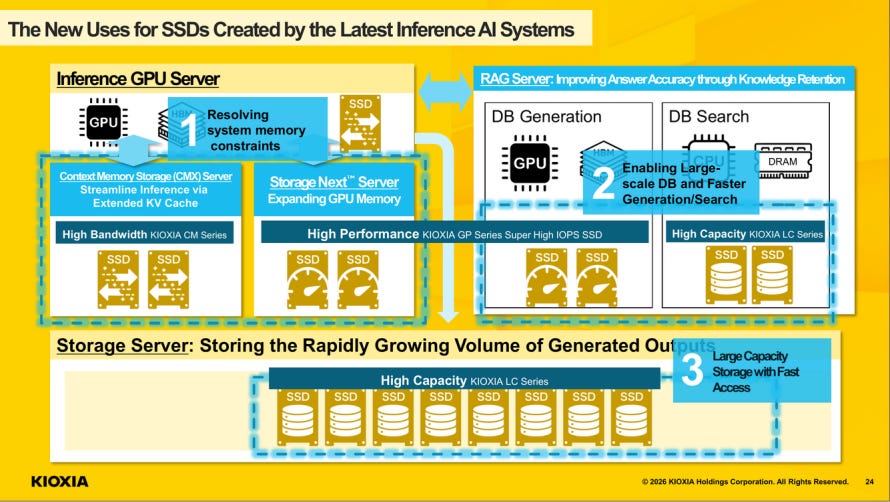

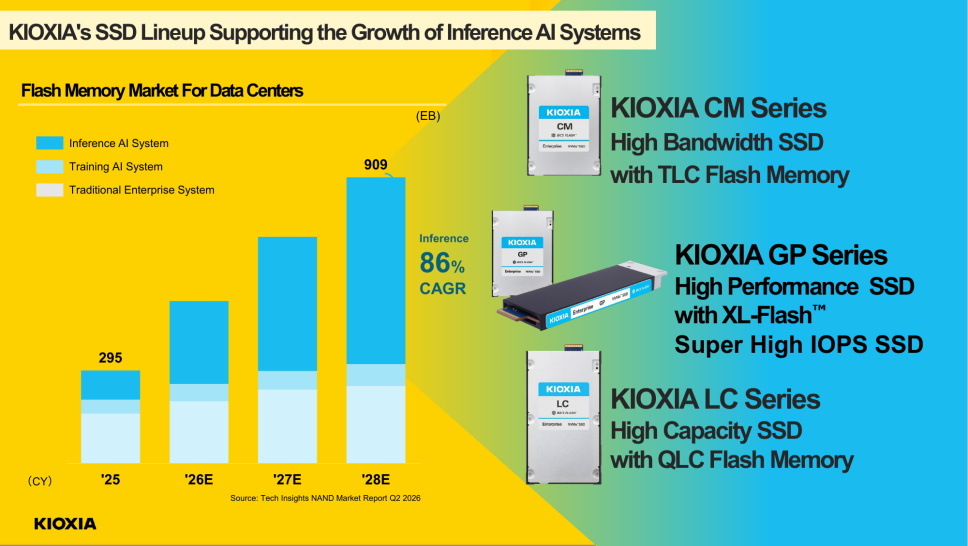

Investor Day Slide 24 — The New Uses for SSDs Created by the Latest Inference AI Systems

The architectural centrepiece of the SSD division’s strategy, illustrating how the evolution of AI inference systems has created three distinct, additive demand vectors for SSDs — each addressed by a dedicated product line. The first use case is resolving GPU memory constraints: as KV Cache grows with the increasing complexity of inference workloads, DRAM alone can no longer keep pace, and the KIOXIA CM Series high-bandwidth TLC SSD enables a Context Memory Storage (CMX) server to extend the GPU’s effective memory pool efficiently. The second use case targets the RAG server layer, where large-scale vector databases must be generated and searched rapidly to improve answer accuracy through knowledge retention — a task Yokotsuka assigned to both the high-capacity KIOXIA LC Series and the high-bandwidth CM Series working in tandem. The third use case addresses the Storage Next architecture, where SSDs transition from a peripheral storage tier into an active extension of GPU memory itself; here the KIOXIA GP Series Super High IOPS SSD, built on XL-Flash, delivers the ultra-low latency and high IOPS throughput required to make that memory-expansion paradigm viable in production. These three server architectures — CMX, RAG, and Storage Next — are not competing but co-existing within every modern inference cluster, meaning that each new generation of AI infrastructure represents a simultaneous, compounding demand opportunity across all three of Kioxia’s SSD families.

SECTION 2 — TECHNOLOGY ROADMAP: BiCS10 + AI SSD PORTFOLIO

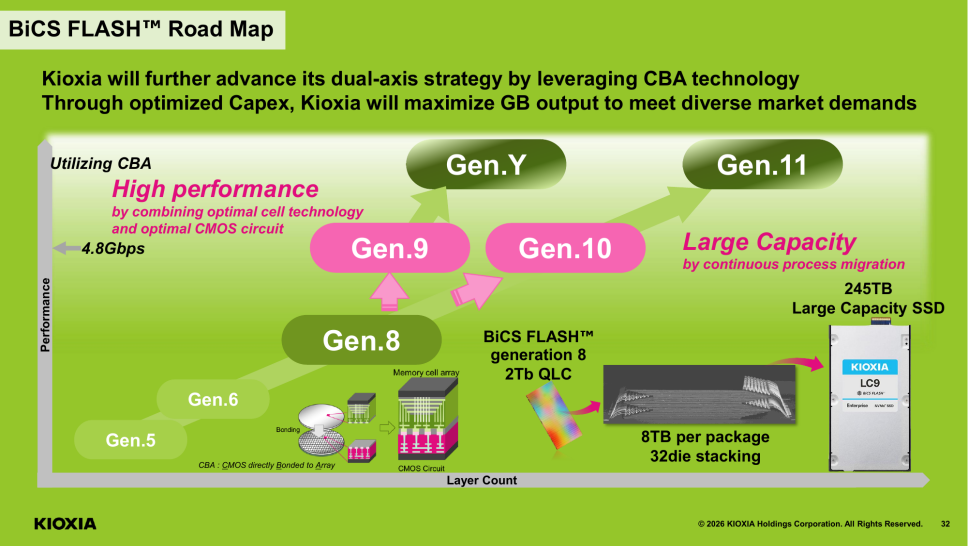

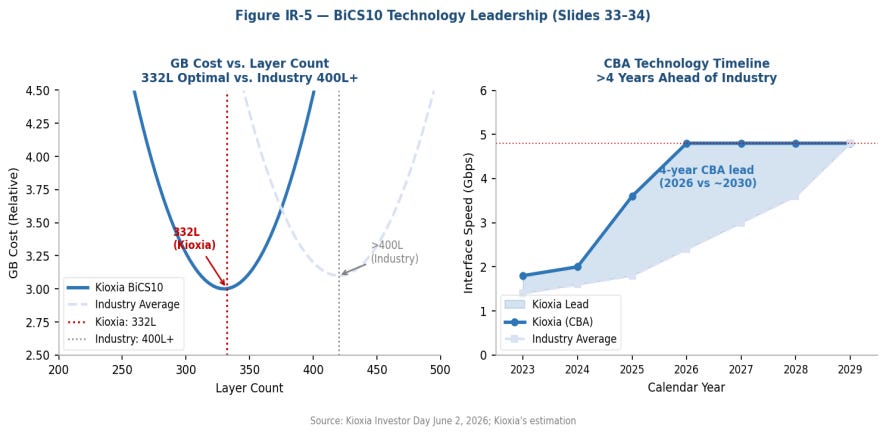

Investor Day Slide 32 — BiCS FLASH Roadmap: Dual-Axis Strategy via CBA (Performance: Gen.9 3.6Gbps → Gen.10 4.8Gbps; Capacity: 245TB SSD today, scaling further)

The dual-axis roadmap: Performance axis advances via CBA from 3.6Gbps (BiCS9) to 4.8Gbps (BiCS10/11); Capacity axis advances via continuous process migration (BiCS8 2Tb QLC → 245TB SSD today, with Gen.10 extending further). CBA bonds CMOS directly to the array, enabling performance gains independent of layer-count increases — the key reason Kioxia’s 332-layer BiCS10 outperforms industry 400+ layer designs.

Figure IR-5 | Source: Kioxia Investor Day June 2, 2026 (Slides 33–34); Kioxia's estimation

Investor Day Slide 35 — BiCS10 Dev Status: On Track | Samples Summer 2026 | Bit Density +59% | Interface +33% to 4.8Gbps | Read Power Eff. +40% | Write Power Eff. +30% vs. BiCS8

Investor Day Slide 28 — SSD Lineup: CM Series (High-BW TLC, NVIDIA CMX) | GP Series (XL-Flash 100M+ IOPS, NVIDIA Storage-Next) | LC Series (245TB QLC, now in mass production)

CM, GP, and LC product lines each address a distinct AI inference bottleneck — KV cache memory, GPU memory extension, and RAG/vector DB storage respectively. The LC series is already in mass production, meaning near-term FY26 revenue contribution is not speculative. The GP series (Super High IOPS using XL-Flash) is the most differentiated product, targeting NVIDIA Storage-Next workloads with 100M+ IOPS performance that current TLC/QLC SSDs cannot achieve.

SECTION 3 — FINANCIAL STRATEGY, SHAREHOLDER RETURNS & VALUATION

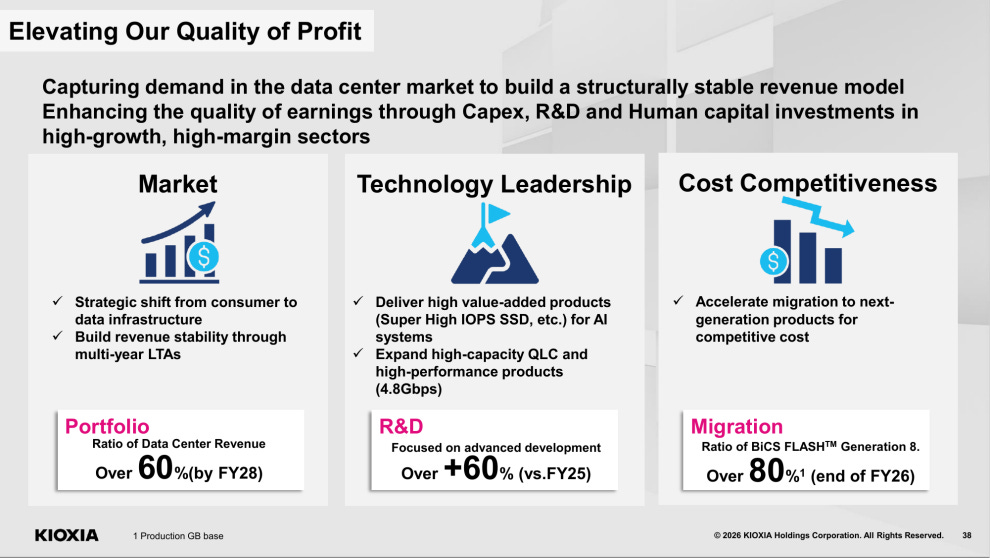

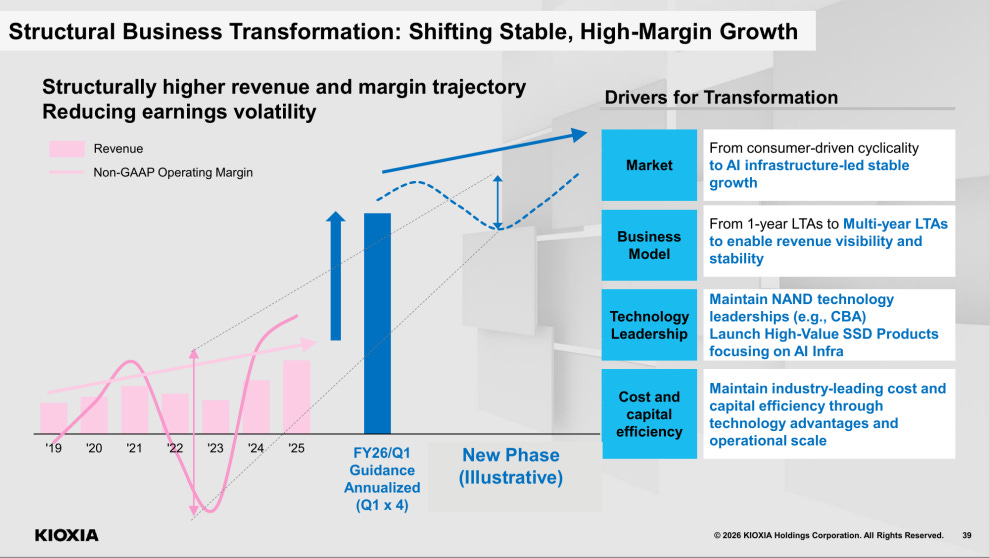

Investor Day Slide 38 — Structural Business Transformation: Consumer-Driven Cyclicality → AI Infrastructure Stable Growth | Multi-Year LTAs | Q1 FY26E OPM: 74% Guided | “New Phase” Trajectory (Illustrative) — drivers: Market shift, LTA model, Technology leadership, Cost/capital efficiency

The ‘Structural Business Transformation’ slide is Kioxia’s most compelling valuation argument. The operating margin trajectory from FY19 through FY25 to the Q1 FY26 run-rate is a phase change: from -30% (FY23 trough) to +37% (FY25) to the guided 74% in Q1 FY26. The annualised Q1 guidance revenue of ~¥7 trillion — far above historical peak revenues — defines the “New Phase.” Four drivers of this transformation: (1) market shift from consumer cyclicality to AI infrastructure stable demand; (2) business model shift from 1-year to multi-year LTAs; (3) technology leadership (CBA) enabling high-value SSD product launches; (4) sustained cost and capital efficiency.

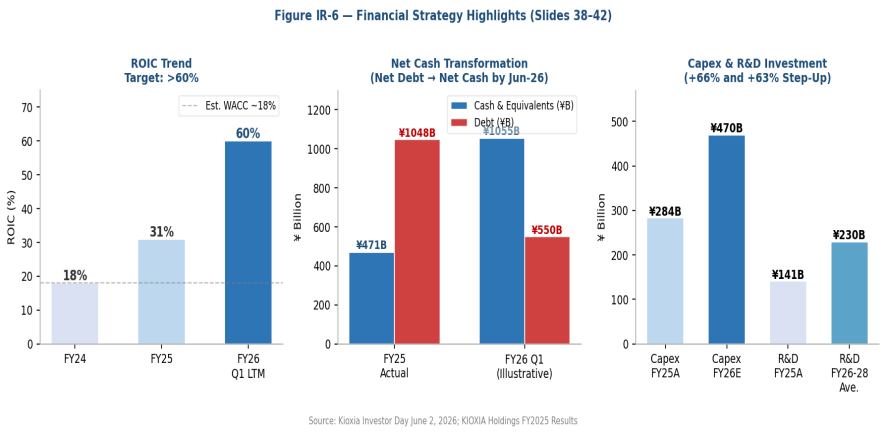

Investor Day Slide 39 — ROIC: FY24 18% → FY25 31% → FY26 Q1 LTM >60% | Target: Best-in-Class Among Manufacturing Companies | WACC ~18% | Only projects exceeding hurdle rate funded | NOPAT / (Equity + Net Debt)

ROIC has improved dramatically: from 18% in FY24 (approximately equal to the ~18% estimated WACC) to 31% in FY25, to a rolling last-12-month ROIC exceeding 60% using FY26 Q1 as the run-rate. The target of >60% sustained ROIC is one of the most ambitious in the global semiconductor industry. CFO Kawamura confirmed that only projects exceeding the investment hurdle rate will be funded — a capital discipline message aimed at calming concerns about excess capex. EPS and FCF per share are described as showing “significant improvement.”

Figure IR-6 | Source: Kioxia Investor Day June 2, 2026; KIOXIA Holdings FY2025 Full-Year Results

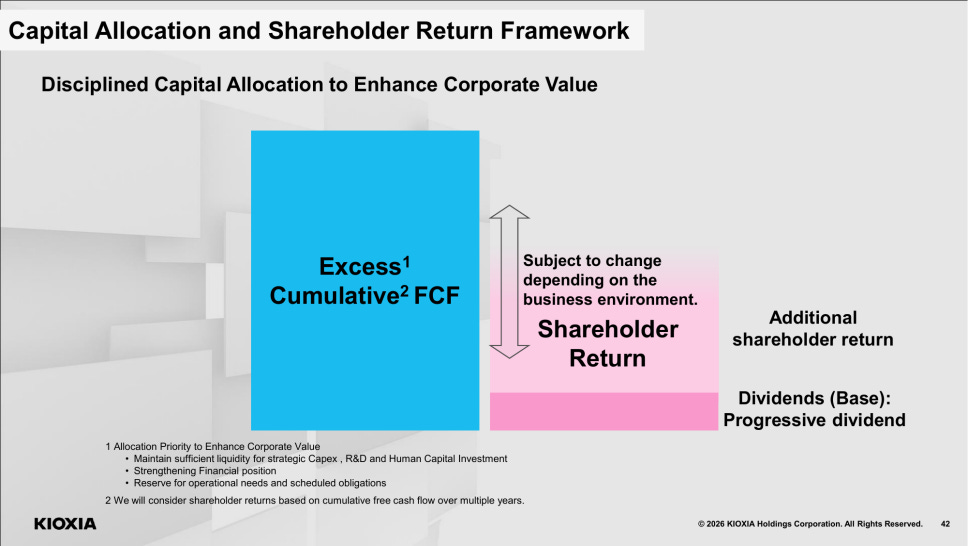

Investor Day Slide 42 — Capital Allocation: Progressive (floor) Base Dividend (FY3/28E) + Additional Returns from Cumulative Excess FCF | Priority: Capex/R&D/Human Capital → Financial Position → Reserve; then Shareholder Returns | DPS FY26E: ¥1,800; FY27E: ¥2,000

The capital allocation framework is the most important new disclosure for institutional investors. Key details from CFO Kawamura: (1) Progressive dividend from FY3/28 — floor that can only be maintained or increased; (2) If cash generation exceeds plan, dividends could begin in 2H FY3/27; (3) If M&A is delayed, all excess FCF could theoretically be returned to shareholders. Our FY27E FCF estimate of ~¥4 trillion annually implies that even a conservative 20–25% allocation to returns would yield ¥800B–¥1 trillion in annual distributions from FY27 — equivalent to a 2–3% yield at current ¥72,500. We expect a formal dividend payout target to be announced with Q1 FY26 results (August 2026).

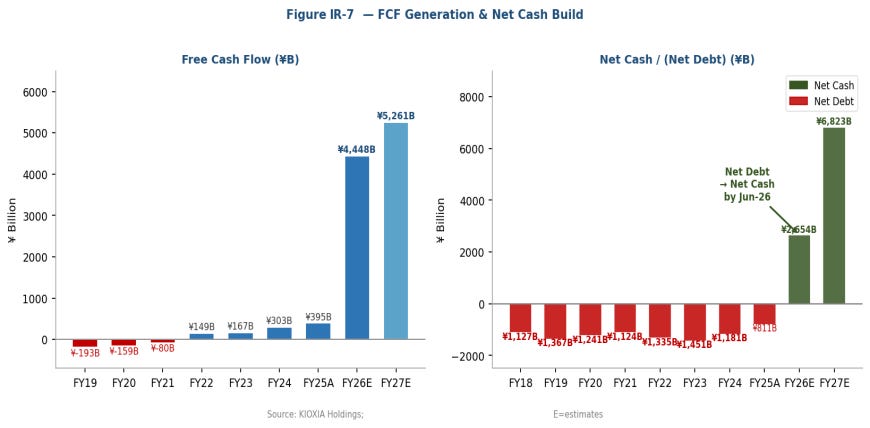

Figure IR-7 — FCF generation and net cash/(debt) trajectory | Source: KIOXIA Holdings;

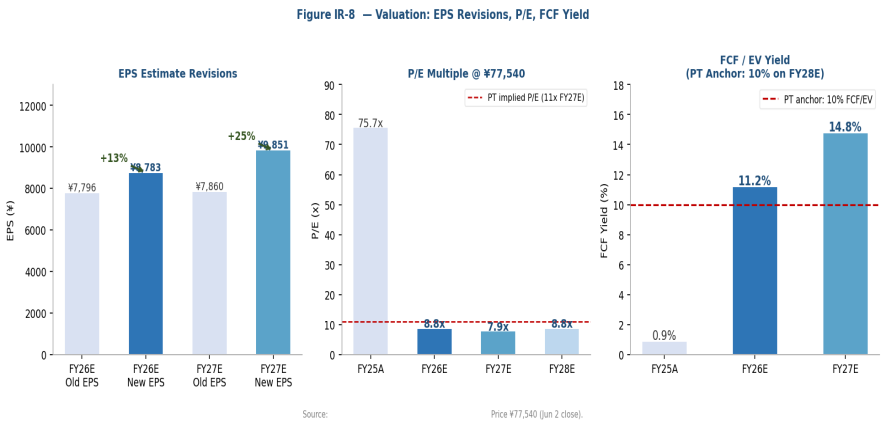

Figure IR-8 — EPS revisions, P/E multiple at ¥77,540, FCF/EV yield (PT anchor: 10% on FY28E)

SECTION 4: PEER COMPARISON — KEY METRICS & POSITIONING

NAND Peer Group — Financial Summary (CY2025 / CY2026E)

Investment Preference Order: (1) Kioxia — best pure-play, cheapest valuation, superior technology lead, massive guidance beat; (2) Micron — US-listed pure play with DRAM diversification and AI optionality; (3) SanDisk — shares JV technology with Kioxia but trades at 2x the valuation; (4) SK Hynix — NAND exposure supplemented by superior HBM/DRAM; (5) Samsung — most diversified, NAND leverage diluted.

DISCLAIMER: This document does not constitute investment advice. Past performance does not guarantee future results. All estimates are subject to change without notice.